_Igor_Stevanovic_Alamy_Stock_Photo.jpg?#)

Struggling with the struggle to get under 5/24 (on Nick’s mind)

I’ve long advocated against over-emphasizing the 5/24 rule and thereby missing out on easy opportunities now for the sake of a shot at a future welcome offer (See: Stop over-valuing 5/24 slots). That’s particularly true when you’re missing out on a more valuable welcome offer now in order to become eligible for a lesser welcome offer […] The post Struggling with the struggle to get under 5/24 (on Nick’s mind) appeared first on Frequent Miler. Frequent Miler may receive compensation from CHASE. American Express, Capital One, or other partners.

I’ve long advocated against over-emphasizing the 5/24 rule and thereby missing out on easy opportunities now for the sake of a shot at a future welcome offer (See: Stop over-valuing 5/24 slots). That’s particularly true when you’re missing out on a more valuable welcome offer now in order to become eligible for a lesser welcome offer later. Despite all that, I’m currently really struggling with a desire to get under 5/24 — and the temptation to go over.

The 5/24 rule

Some banks will not approve you for a new credit card if you have opened too many new accounts within the past 24 months.

Chase is anecdotally known to deny applicants who have 5 or more new credit card accounts with any issuer in the previous 24 months. Most business credit cards are not included in this count (even Chase ones), but you’ll need to have 4 or fewer new credit card accounts within the past 24 months if you want to get approved.

To determine your 5/24 status, see: Easy Ways to Count Your 5/24 Status. The easiest option is to track all of your cards for free with Travel Freely.

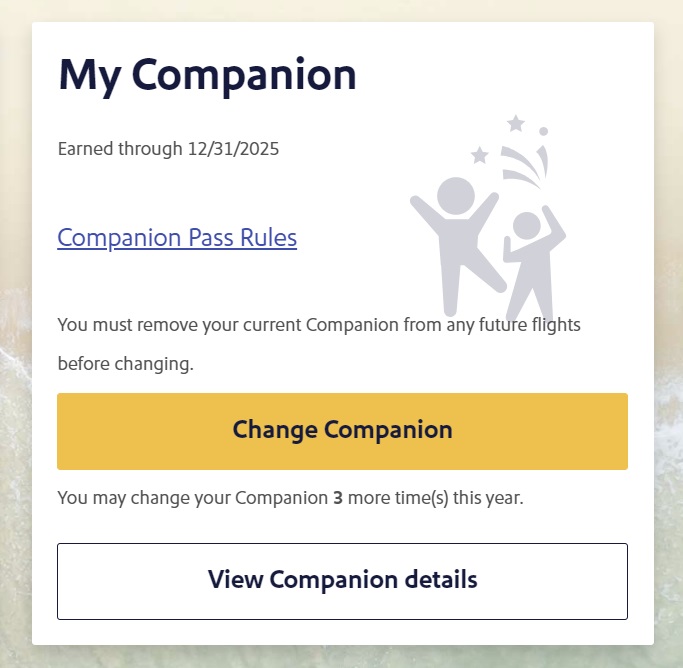

I really want a Southwest Companion Pass

My wife and I have had a Southwest Companion Pass in our household for more than a decade. While we love fancy international business or first class award tickets as much as anyone, my family almost exclusively flies Southwest when we travel domestically as a family (for a variety of reasons),

In the beginning, our first couple of Companion Passes came via the Southwest Rapid Rewards Shopping portal. Back in those days, I was buying and reselling products. I think I may have lost a little bit of money on the resale of the products I bought to earn my first companion pass, but I earned enough points for the Companion Pass in one fell swoop, which more than negated the small loss.

In the years since, the Rapid Rewards shopping portal just hasn’t been very interesting. I can’t remember the last time that the Rapid Rewards shopping portal was offering the best rate of return for an item I wanted to purchase, so we have turned to earning points via credit card.

Eventually, my wife got both a Southwest consumer credit card and a Southwest business credit card, earning a Companion Pass from the welcome bonuses. In subsequent years, she’s been able to pick up enough referrals for the card to re-earn the Companion Pass every other year, so we’ve had that one Companion Pass in our household year after year for a long time.

However, now that we have two kids, two Companion Passes would be ideal so that we could be getting not one but two free seats every time our family of four flies Southwest.

Unfortunately, I do not have a Southwest credit card of my own. I’d love to be able to get a Southwest consumer card and a Southwest business card, but I need to get under 5/24 if I’m to do it.

Currently at 6/24 and would go under 5/24 in August

I’m currently sitting at 6/24. The following are when my oldest “new” accounts will drop off the count:

- August 1, 2025

- August 1, 2025

- October 5, 2025

- December 12th, 2025

In other words, if I didn’t open another card between now and July, I’d end up at 4/24 by August 1st. I’ll drop one further to 3/24 at the beginning of October, which is historically a great time for Southwest cards.

Cards I want right now (Should I keep waiting?)

While I want a Southwest Companion Pass, I’m struggling with the idea of waiting 5 more months to be eligible. That is in large part because of several current “wants”.

Hawaiian Airlines Mastercard

| Card Offer and Details |

|---|

70K Miles ⓘ Non-Affiliate 70K miles after $1,000 spend within first 90 days. Use code 000150 for this offer$99 Annual Fee Information about this card has been collected independently by Frequent Miler. The issuer did not provide the details, nor is it responsible for their accuracy. Recent better offer: 70K miles after one purchase within first 90 days Earning rate: 3X Hawaiian Airlines ✦ 2x gas, dining, and grocery stores ✦ 1x everywhere else Card Info: Mastercard World Elite issued by Barclays. This card has no foreign currency conversion fees. Noteworthy perks: Two free checked bags when flight is booked through Hawaiian Airlines ✦ One time 50% off companion ticket ✦ $100 off a companion ticket for roundtrip coach travel between Hawaii and North America on Hawaiian Airlines at each account anniversary |

I really want a Hawaiian Airlines Mastercard because my family has a stash of Alaska/Hawaiian miles spread across several family member accounts. We flew a “paid” British Airways business class fare a couple of years ago (we used the Amex Business Platinum’s pay-with-points rebate to book), so my wife and one of my sons earned a bunch of Alaska miles from that. Then we similarly flew a “paid” Hawaiian Airlines business class fare (using Business Platinum points) last year and all four of us earned over 13,000 Hawaiian miles on that flight.

The Hawaiian Airlines Mastercard allows the cardholder to combine miles with others for free. If I got this card, I could move miles from all of our family accounts to Hawaiian (from Alaska to Hawaiian first as necessary) and then as a cardholder we could move the all of the Hawaiian miles in my wife’s account and both sons’ accounts into my Hawaiian account and then on to my Alaska account. The end result being around 400,000 Alaska miles in a single account, which is far more useful than having 13,200 Hawaiian miles in one son’s account and around 50K between Alaska and Hawaiian in another son’s account, etc.

Note that I could accomplish this with either the Hawaiian consumer card or the Hawaiian Business card. A notable perk of the business card is that it wouldn’t add to my 5/24 count — it would essentially fly under the radar.

However, the intro bonus is 20,000 miles better on the consumer card, the spending requirement is lower, and Barclays can be weird on approvals for their business cards. I could try for the business card, but if I weren’t concerned about 5/24, I’d be going after the consumer card. I somewhat regret not getting the consumer card when it offered 70,000 miles after first purchase (you now need to spend $1,000 in the first 3 months to trigger the bonus).

Finally, of key importance here is the fact that we don’t expect the Hawaiian cards to be available forever, Current speculation is that Barclays will probably stop taking applications for the Hawaiian cards by the time the programs merge, which is expected to happen around the middle of this year. Will they stop taking applications sooner than that? Will the card continue to be offered beyond summer 2025? We don’t know. But I believe that my window of opportunity on this card is going to be measured in months at best.

Capital One Venture Rewards credit card

| Card Offer and Details |

|---|

75K Miles ⓘ Friend-Referral 75k miles after $4k spend within first 3 months. (Rates & Fees)$95 Annual Fee Alternate Offer: Airport Kiosk offer of 80K miles after $4K spend in the first 3 months See this post for details. Information about this card has been collected independently by Frequent Miler. The issuer did not provide the details, nor is it responsible for their accuracy. Recent better offer: Expired 9/9/24: 75K after $4K spend in 3 months + $250 Capital One Travel credit in first cardholder year FM Mini Review: This card earns 2 "miles" per dollar, which are worth exactly 1 cent each toward travel. This makes the return on spend similar to a 2% cash back card (though in this case you must redeem your miles to offset travel in order to get 1 cent per mile). One big advantage over cash back: Capital One allows transfering their "miles" to airline miles & hotel points. Click here for our complete card review Earning rate: 2X miles everywhere ✦ 5X miles on hotels, vacations rentals and rental cars booked via Capital One Travel Card Info: Mastercard issued by CapOne. This card has no foreign currency conversion fees. Noteworthy perks: Receive up to $120 application fee credit for Global Entry or TSA PreCheck® ✦ Redeem miles for travel at value of 1 cent per mile ✦ Convert "miles" to airline miles & hotel points ✦ No foreign transaction fees |

This pick will surprise some, but it will make sense: I want to open a new Capital One Venture (or maybe Venture X?) card. My wife already has a Venture X card and I have an old VentureOne card, either of which allows for transfers to partners. Since there is no fee to add an authorized user on a Venture X card, it wouldn’t ordinarily make much sense to have a second Venture or Venture X card in a single household.

However, for starters, there’s the welcome bonus, which is decent on either card at 75,000 transferrable points after $4K in purchases. But that’s not the whole story. We’re currently collecting reader referral links for the Venture card here and using them on our Best Offers page. Cardholders can earn up to 100,000 Capital One miles per year for referring others (I believe it’s 20K miles per referral on the Venture or 25K per referral on the Venture X, so this maxes out after 4 or 5 referrals). I imagine that I could probably end up with 100,000 extra miles from referrals, making this feel more like a 175K bonus (and it would give me capacity for referrals in future years as well). That obviously changes the math significantly.

It’s worth noting that the Venture X is the better deal mathematically, but we need another $395 annual fee like we need a hole in the head, so I’m leaning toward wanting the Venture just to keep things simple.

Amex Green Card

| Card Offer and Details |

|---|

40K points ⓘ Friend-Referral 40K after $3K spend in first 6 months. Terms apply. See Rates & Fees$150 Annual Fee Information about this card has been collected independently by Frequent Miler. The issuer did not provide the details, nor is it responsible for their accuracy. Recent better offer: 60K after $3K spend in first 6 months + 20% off travel and transit purchases for first 6 months. [Expired 8/21/23] FM Mini Review: This card is worth considering as your go-to travel card, but only if you value its CLEAR and Lounge Buddy credits. Also note that Amex cards continue to have limited acceptance in many international destinations. Click here for our complete card review Earning rate: ✦ 3X on travel & transit (including flights, hotels, taxis, and rideshares) ✦ 3X dining ✦ 1X points on other purchases. Terms apply. See Card Info: Amex Pay Over Time Card issued by Amex. This card has no foreign currency conversion fees. Noteworthy perks: $199 CLEAR credit annually Terms Apply. |

I also want to get an Amex Green card. That doesn’t make much sense on the surface given the fact that it features a comparatively weak welcome bonus and a relatively weak set of benefits for its annual fee.

Here’s my situation: I have a consumer Platinum card that I failed to cancel within 30 days of the annual fee posting. I’ve now used my various 2025 fee credits on the Platinum card. Since more than 30 days have passed since the annual fee was billed, if I cancel the card now, I won’t receive any refund of the annual fee. However, if I downgrade the Platinum card, I’ll get a prorated refund of the annual fee that will correspond with the number of months left in my cardmember year (~10 months, so I’ll get about $579 back). Then, I’ll pay a prorated fee on the card to which I downgrade.

From the Platinum card, my only downgrade path options are to downgrade to an Amex Gold card (which I currently have) or an Amex consumer Gold card. Since the Green card has the lower annual fee, it makes more sense to downgrade to a Green card. I’d be charged the prorated fee for 10 months of the Green card (about $125). In the end, I’d net about $454 back if I downgrade rather than cancelling (again, if I simply cancel my Platinum card, I won’t get anything back).

My problem is that I’ve never had the Amex Green card before. Amex application terms typically say that you are not eligible for the welcome bonus if you have or have had the card before. If I downgrade to the Green card, the application terms would mean that I may never be eligible for the welcome bonus on the Green card in the future since I will have had the card if I downgrade to it.

It might therefore make sense for me to apply for a Green card first, before downgrading my Platinum card. That way, I could be eligible for the welcome bonus on the Green card.

What I think I should do is open an Amex Green card now. Then, in a few days, I could downgrade my Platinum card to a second Green card. I’d end up with two (largely useless) Green cards, but I’d earn the 40,000-point welcome bonus (at the time of writing) on the new one and get a net $454 back on the downgraded one.

Essentially, if I don’t apply for the Green card now without first applying for it, I’m costing myself a shot at 40,000 points.

Other cards

I should note that the above cards aren’t the only ones I want. I’d also like to get a Hilton Honors Surpass card in our household (we haven’t had one in many years) and I’m really interested in the U.S. Bank Smartly card as I think we could meet requirements to make that a 3%-everywhere cash back card. Those aren’t the only other cards I want — my point here is that I’ve been waiting on other opportunities as well.

Do I push off falling under 5/24 for a few months? Do I give up on it entirely for 2025?

This all brings me to a dilemma: do I hold the line and try to avoid opening any consumer cards until I fall below 5/24 in July, or do I move forward and open a couple of new cards now?

Since the best time to open Southwest credit cards tends to be late in the year, I would have envisioned waiting until October to try to open Southwest cards, looking to earn the welcome bonuses for one Southwest consumer card and one Southwest business card in January 2026 so that I could have a Companion Pass for almost two full years (the rest of 2026 and until December 31, 2027). Since I wouldn’t be under 5/24 until about August 1st, I likely couldn’t earn the Companion Pass in time for our summertime domestic travel this year (since I’m not eligible to apply now under the current referral offer). In short, I guess it makes sense that I don’t need to be under 5/24 until October.

With that decided, I could afford to open one new card now. That would put me at 7/24 for now, but around August 1st, I would drop back to 5/24 when the two oldest accounts fall off of my 5/24 count. Then, in October, the next oldest account would drop off, knocking me down to 4/24 — at which point I could apply for Southwest cards. That seems like it could work.

My next oldest card after the one that falls off in October comes off in December. If I can wait until December to get my Southwest credit cards, I could add one more new account now, bumping myself up to 8/24 right now, dropping to 6/24 in August, 5/24 in October, and back down to 4/24 in December.

I’m a little bit hesitant to wait until December since the welcome offer sometimes changes in early December, but since I could probably pick up some referrals even if the welcome offer is unideal, I think that’s not a bad bet. I think that opening two consumer cards right now seems reasonable enough.

But which two?

Narrowing down the field

As you can see above, the question comes down to which card to eliminate from the trio of cards I want right now if I want to earn a Companion Pass.

I think that based on the number of total transferable points I can earn, I should probably try for a Venture card first. The combination of welcome bonus and potential referral points, both this year and in the future, is worth so much more than the other bonuses I’m considering. In fact, if I got this card and happened to get the 4 or 5 referrals necessary to max out the bonus, I could have enough miles to erase $1,750 in travel, or I could get far more value transferring to airline partners. This bonus might be more valuable to me than a Companion Pass. I think it should be the first card I try for now. (Note that I’m not recommending that others make this card a top priority — my situation here is fairly unique).

Capital One is known to be very fickle with folks who already have a lot of cards. I think there’s certainly a chance that I won’t get approved for a card with Capital One based on the fact that I have so many accounts open with other banks. If I don’t get approved for a Venture card, then I could go after the other two cards I’m considering. If I get approved for a Venture card, I have to decide whether to get a Hawaiian card or a Green card now.

To be clear, I’ll also still consider business cards between now and when I fall under 5/24 since most business cards do not add to one’s 5/24 count, but I’ll try to hold off on being tempted by other consumer cards until I fall back under 5/24 in December.

The card I need to chop from my strategy is the Amex Green card. The current welcome offer on the green card is significantly less valuable than the welcome offer on the Hawaiian card. And while I might not be eligible for the bonus on a Green card in the future after I downgrade my Platinum card, Amex sometimes allows people top earn a welcome offer on a card they’ve had before even though terms state that they may not. That means there’s a chance I could possibly still get the welcome bonus on a Green card “someday”. I think that the Hawaiian card will likely go away forever at some point this year. It’s a much more time-limited opportunity in my opinion.

Final decision

I think I’ve convinced myself to go ahead and go for a Venture card and a Hawaiian card now as that will only push back my Southwest card eligibility by a couple of months, likely to the time of year when I would have been considering applying anyway. I’ll potentially forgo my shot at an Amex Green card bonus, but I continue to earn a lot of Membership Rewards points from business card bonuses as well as category bonuses on my existing Amex cards, Rakuten, referrals, etc. I do want to become eligible for a Southwest Companion Pass and I’m willing to sacrifice a shot at 40,000 Amex points to open up the possibility of being eligible for Southwest cards later this year, but I don’t think I should sacrifice the opportunity to get the other cards I want now even if it means pushing the Southwest cards down the line a few months.

The post Struggling with the struggle to get under 5/24 (on Nick’s mind) appeared first on Frequent Miler. Frequent Miler may receive compensation from CHASE. American Express, Capital One, or other partners.